In a previous post, Red Flags of Fraud, I wrote about 5 red flags you should be on the lookout for in your employees’ behavior to prevent fraud in your company.

These are:

- An employee refuses to take vacation and rarely takes personal or sick days

- An employee gets annoyed at reasonable questions or offers unreasonable explanations

- An employee wants to remain in his or her current position

- An employee exhibits behavioral changes, undergoes a sudden change in lifestyle or has financial difficulties

- An employee has unusually close relationships with vendors

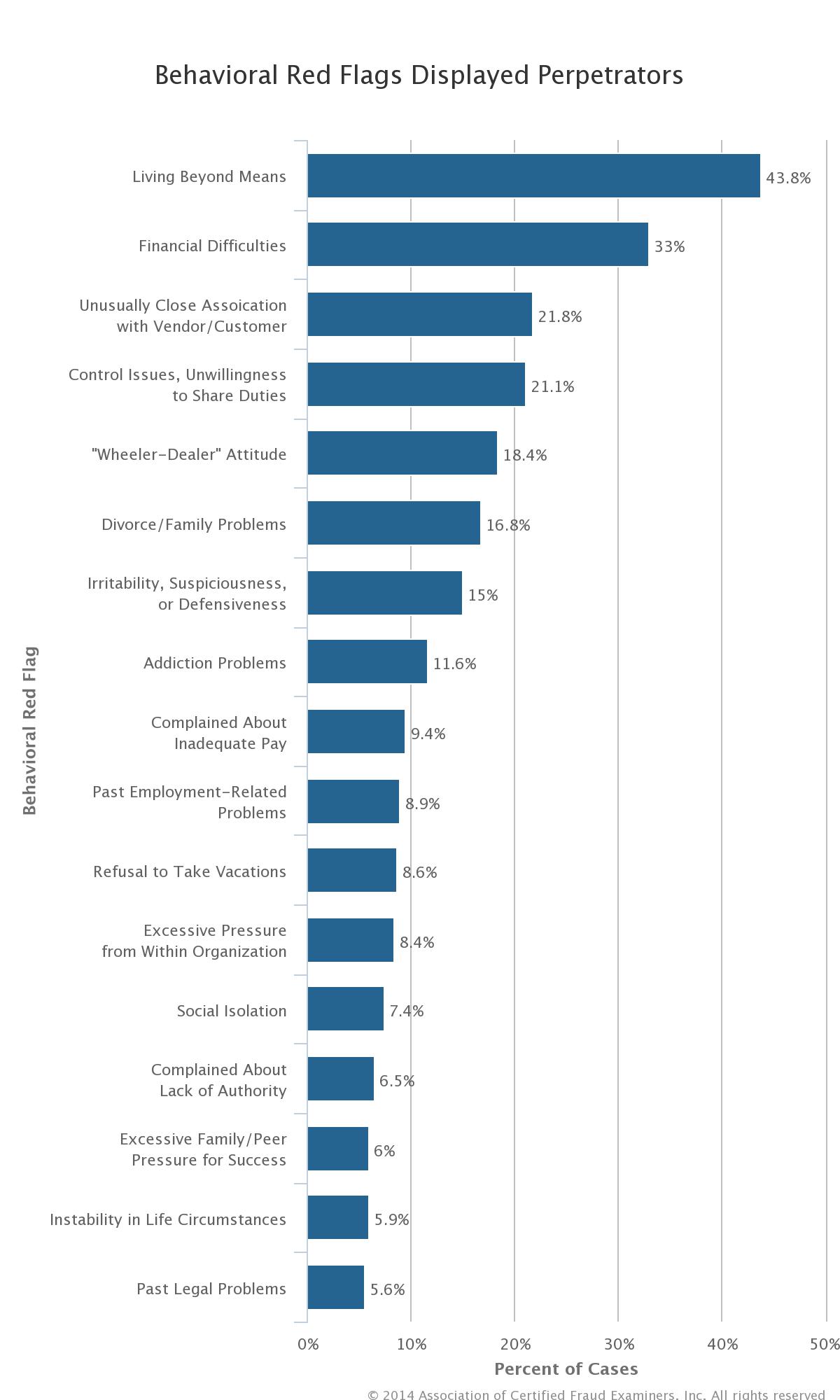

The 2014 Global Fraud Study done by the Association of Certified Fraud Examiners found of all cases they analyzed, 92 percent of the people who committed fraud exhibited certain behavioral traits, all of which are listed above.

The top two traits the study found are Living Beyond Means (43.8 percent) and Financial Difficulties (33 percent), as listed in #4. I’d like to expand on these two behaviors, as they may be harder to detect than the others above and on the chart you see here.

The top two traits the study found are Living Beyond Means (43.8 percent) and Financial Difficulties (33 percent), as listed in #4. I’d like to expand on these two behaviors, as they may be harder to detect than the others above and on the chart you see here.

If an employee begins to talk about financial difficulties, too much credit card debt or high medical bills, that’s the time to pay a bit more attention to him. Pressure from financial problems due to things such as overspending, a divorce or health problems can set the stage for an employee to consider fraud as a way out of his difficulties.

Another behavioral change to note is when an employee who may have previously complained about being overworked, underpaid or passed over for a promotion no longer talks about workplace issues and seems more content although nothing has changed.

If she is committing fraud, she may feel that she is evening the score and taking what she considers is due to her. She now feels happier in the workplace.

Changes in lifestyle can be a bit trickier to determine. An employee may start driving an expensive new car, talk about a new second home or take high-end vacations. She may chat about moving to a new home in an upscale neighborhood or bring in photos of a new boat.

It can be tricky to question someone about these purchases and where the money came from. And they could be explained by claiming to have gotten an unexpected inheritance, or a spouse with a new high-paying job.

Or, as often happens, the money is spent somewhere the employee would not be eager to share at his workplace. Michael Dennehy embezzled over $1.7 million from Bexar Waste in San Antonio by forging company checks for more than six years. He admitted that he spent it on escort services and gambling. As a married father of five, he probably wasn’t sharing those stories in the break room.

Make observing behavioral changes part of your fraud prevention program and share this information with your management team, so they can be vigilant about these behaviors.

Fraud prevention is vital for any business. The median loss caused by fraud in the ACFE study was $145,000, with 22 percent of the cases costing a company more than $1 million.

Come back next time when I’ll discuss why small businesses are disproportionately affected by fraud and what small business owners can do to protect themselves.